Understanding The OTCBB

What is the OTC Bulletin Board?

What is the OTC Bulletin Board?

The OTC Bulletin Board is an electronic, interdealer quotation system that displays real-time quotes, volume information for over-the-counter equity securities (those securities not listed on the NASDAQ or a national securities exchange), and last-sale prices for many equity-securities in the United States.

The OTC Bulletin Board is a service delivered to broker-dealers who may subscribe to the system for a yearly fee. Once the service is acquired, a broker-dealer or financial institution can effectively look up prices or enter quotes for OTC securities.

The Financial Industry Regulatory Authority is the administrative and authoritative body responsible for running and overseeing the OTCBB. That being said, FINRA announced in September of 2009 that the agency would be selling the OTCBB. The sale was initiated because competitors—like the Pink OTC Markets who are rumored to purchase the OTCBB—are stripping the OTCBB of its listing powers. Prior to 2008, the OTCBB collected 100% of quotes, but this number has declined due to the rise in competition.

The OTCBB is not part of the NASDAQ stock exchange; however, all companies quoted or listed on the OTCBB must satisfy the filing and full reporting requirements of the SEC. Although regulations exist, the companies listed on the OTCBB possess no responsibility to report specifics associated with a market capitalization, a minimum share price, and corporate governance. That being said, companies may be “de-listed” from the OTCBB for falling below a minimum share price, a minimum capitalization or other requirements that end up being quoted on the OTCBB.

Those stocks not listed or quoted on the OTCBB (stock of non-reporting companies that do not possess current SEC filings) may be quoted in the Pink Sheets. The majority of companies listed on the OTCBB are dually quoted, meaning they are listed on both the OTCBB and the Pink Sheets.

The OTCBB is an electronic trading service offered by the National Association of Securities Dealers. Companies listed on the OTCBB are required to file current financial statements with either the SEC or a banking/insurance regulator.

What kind of Stocks are listed on the OTCBB

Those stocks traded in OTC markets (such as the Pink Sheets or the OTCBB) typically possess minimal market capitalization.

Stocks traded and quoted on the OTCBB possess low trade volumes and are typically classified as microcaps or penny stocks. As a result of this classification, the majority of retail and institutional investors will avoid the stocks listed on the OTCBB due to the risks associated with share price manipulation and the greater potential for fraud.

Due to the aforementioned risks, the Securities and Exchange Commission commonly issues warnings to investors to be aware of manipulation and fraud schemes associated with the companies listed on the OTCBB. As a result of this investor skepticism, most companies will seek listing on more established marketplaces such as the NYSE, AMEX, or NASDAQ.

What is a Prospectus?

What is a Prospectus? What is Global Finance?

What is Global Finance? What is the International Finance Corporation?

What is the International Finance Corporation?

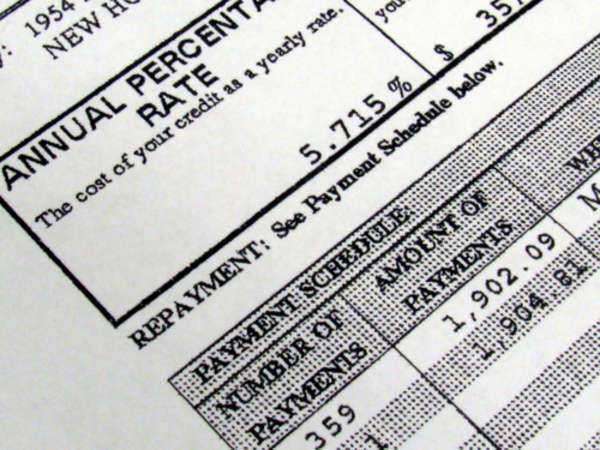

What does APR mean?

What does APR mean? What is a Capital Gain?

What is a Capital Gain? What does Amortization mean?

What does Amortization mean? What is Equity?

What is Equity? What is the FOREX Market?

What is the FOREX Market?